Hi ,

I hope you and your family are safe and well. Here are some important home loans, property and tax stories:

- Refinancing tops $20bn

- How interest rates have evolved over the past 18 months

- How govt is helping new buyers

- Tax deadline nears

Read more below.

With lots of people coming off fixed rates right now, it’s no surprise that an enormous amount of refinancing is occurring, as borrowers look to switch to lower-rate loans.

The latest Australian Bureau of Statistics (ABS) data has revealed that borrowers did $20.60 billion of refinancing in August – which was 3.9% lower than the month before but 12.4% higher than the year before.

Meanwhile, the ABS also revealed that the value of all new home loan commitments in August was $24.82 billion, which was 2.2% higher than the month before.

Owner-occupier borrowing rose 2.6% to $16.07 billion, while investor borrowing rose 1.6% to $8.75 billion.

That said, home loan activity has fallen on a year-on-year basis:

- Total borrowing down 9.4%

- Owner-occupier down 12.5%

- Investor down 3.0%

The interest rate environment has changed a lot recently, and the level of competition in the mortgage market is fierce, so there are a lot of great refinancing deals available – including with quality smaller lenders you may be unfamiliar with.

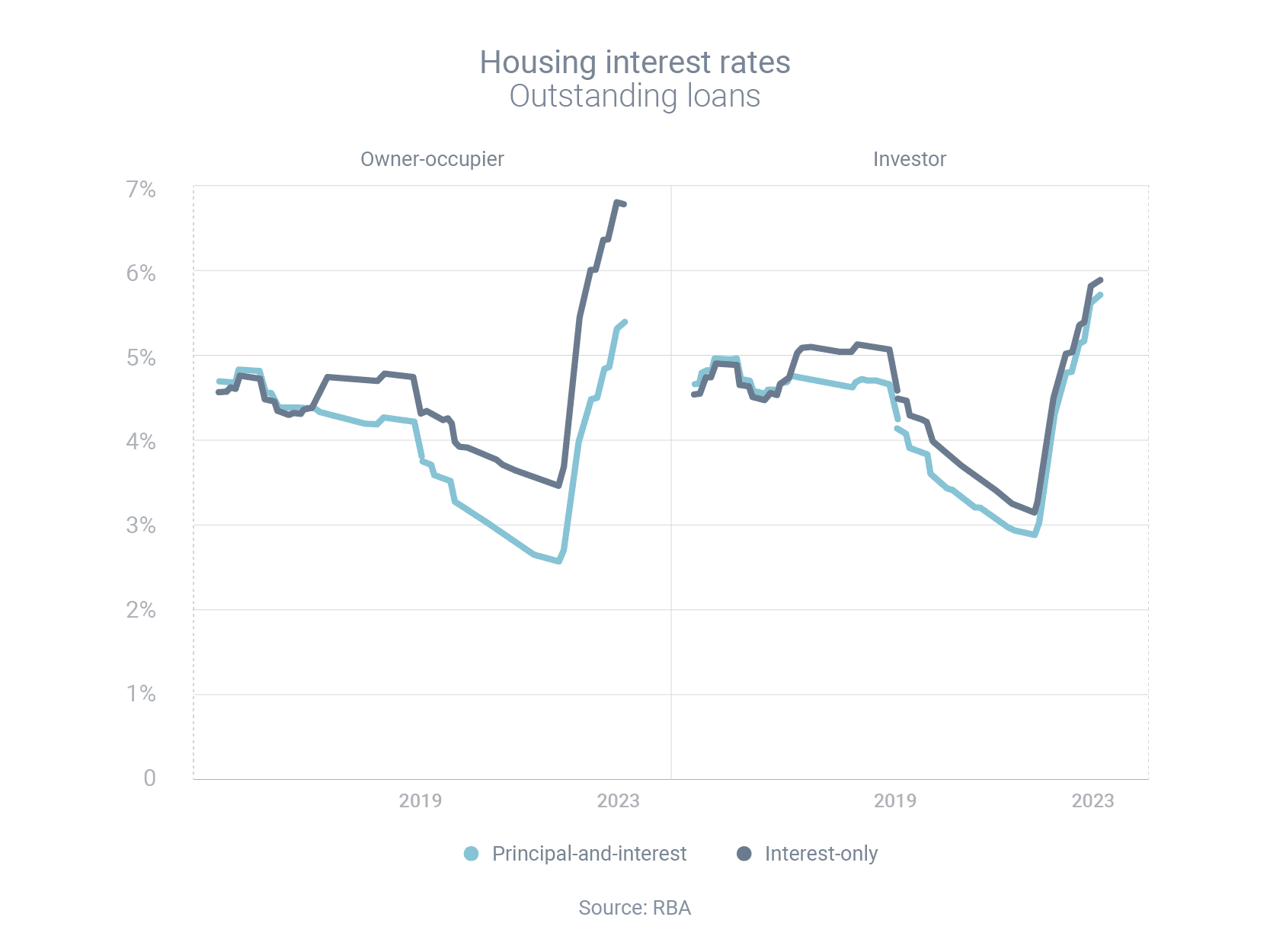

The latest Reserve Bank of Australia (RBA) data has shown the impact the RBA’s cash rate rises have had on the mortgage market.

The key is to compare average interest rates for all outstanding loans in April 2022 – the month before the first rate rise – and August 2023 – the most recent month for which we have data.

During that time, the RBA increased the cash rate by 4.00 percentage points. Interest rates for outstanding loans have, on average, increased by less than that amount, in part because some loans were fixed at lower rates.

For owner-occupied loans, rates have increased by an average of:

- 2.82 percentage points for principal-and-interest loans

- 3.31 percentage points for interest-only loa

For investment loans, rates have increased by:

- 2.83 percentage points for principal-and-interest loans

- 2.73 percentage points for interest-only loans

Future interest rate hikes can’t be ruled out. The conflict in the Middle East may lead to higher oil prices, and therefore higher petrol prices and higher inflation. In the RBA’s cash rate meeting earlier this month, board members noted that “some further tightening of policy [i.e. rate rises] may be required should inflation prove more persistent than expected”, according to the meeting minutes.

A new report, from Housing Australia, has revealed that about one in three of all first home buyers in the 2022-23 financial year used the federal government’s Housing Guarantee Scheme (HGS) and its three different assistance programs.

Here’s what the typical participant looked like, according to Housing Australia:

- First Home Guarantee: the median participant was in the 30-34 age bracket, had a household income of $76,000 and bought a property worth $459,000.

- Regional First Home Buyer Guarantee: participants were aged 25-29, earned $71,000 and bought a $389,000 home.

- Family Home Guarantee (for single parents): participants were aged 35-39, earned $70,000 and bought a $422,000 home.

Meanwhile, Housing Australia is the name of the new agency that has just replaced the National Housing Finance and Investment Corporation and assumed its responsibilities.

Housing Australia has not only taken control of the HGS, but also the National Housing Infrastructure Facility, which provides loans and grants for critical infrastructure to unlock and accelerate new housing supply.

The Australian Taxation office (ATO) has reminded taxpayers to lodge their taxes by the October 31 deadline or engage with a registered tax agent to avoid late lodgment penalties.

If you have simple tax affairs, you can lodge online, often in under 30 minutes, through the myGov portal. Most of the information you need will already be pre-filled – just check it’s correct, add any additional income and claim your legal deductions.

The ATO has also stressed the importance of making sure any claims you make for work-related expenses are accurate, which means you can’t just automatically copy/paste the previous year’s claims.

“We want people to get their deductions right on the first go and claim what they are entitled to – nothing more, nothing less. We have a series of 40 occupation and industry-specific guides which you should have a look at,” ATO assistant commissioner Rob Thomson said.

“It may be tempting to boost your refund by leaving out income or inflating your deductions – but remember, we have sophisticated data analytics that will pick up returns that look suspicious.”

Thanks for reading. If you or your family need advice about home loans or refinancing, I'm here to help.

Kind Regards,Mark Mellick

(02) 9315 7749