Hi ,

Friendly reminder not to leave your Christmas shopping too late! As we approach the end of the year, here’s what’s happening in the home loans and property markets:

- Home loans activity rises

- Fixed-rate transition continues

- Property market keeps growing

- Bank funding costs increase

Read more below.

There’s been a big rise in home loans activity over the course of the year, with investors leading the way.

Between February and September, the total volume of mortgage commitments rose 9.5% to $25.0 billion, according to the latest data from the Australian Bureau of Statistics.

Owner-occupied borrowing climbed 6.1% to $16.1 billion, while investor borrowing jumped 16.0% to $9.0 billion.

-

The number of loans taken out by owner-occupier first home buyers increased significantly between February and September, rising 18.4% to 9,213 loans.

-

Refinancing with external lenders fell 7.1% to $18.5 billion, although that figure was still well above the long-term average.

-

Borrowing for alterations, additions and repairs increased 9.4% to $502 million.

The great transition of the mortgage market, from having a heavy share of fixed-rate loans to now being dominated by variable-rate loans, has gathered pace, according to Reserve Bank data.

During 2020 and 2021, when interest rates fell to record-low levels, enormous numbers of borrowers took out two-year and three-year fixed loans at very low interest rates. Many of those loans then expired as rates started rising, meaning that many borrowers have been reverting from ultra-low fixed rates to significantly higher variable rates.

“The fixed-rate share of total outstanding housing credit declined to 22% in September, well below its peak of just under 40% at the start of 2022,” the Reserve Bank reported in its recent Statement of Monetary Policy.

Over recent months, the number of fixed loans that have expired have outweighed the number of new fixed loans that have been initiated, by a ratio of more than five to one.

“Most of the remaining fixed-rate loans are expected to expire by the end of 2024,” according to the Reserve Bank.

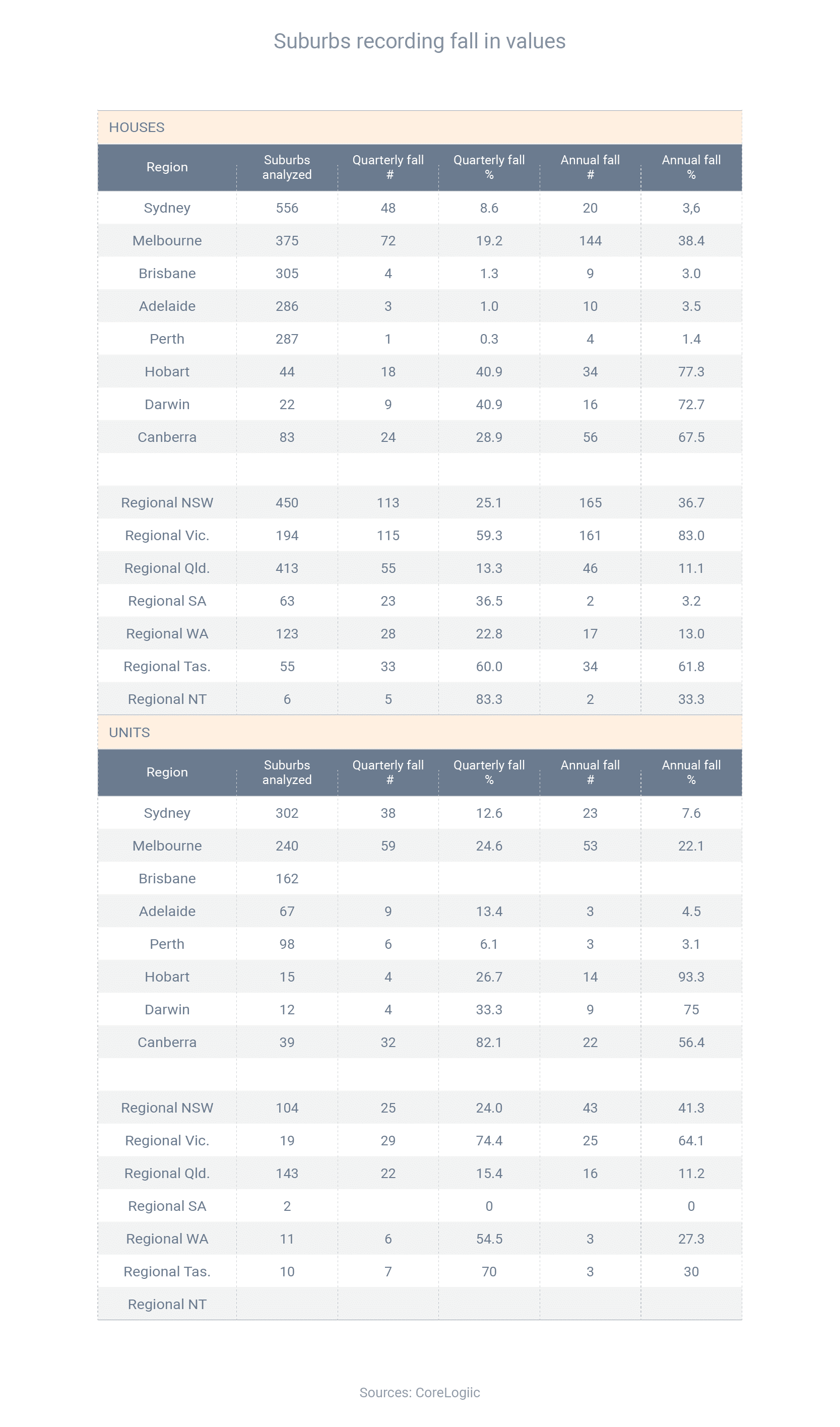

A new report from CoreLogic has found that median property prices increased in 82.4% of local markets in the three months to October, based on a sample of 4,506 suburbs across Australia.

That included price increases in 83.1% of house markets and 80.6% of unit markets.

Focusing just on house markets, prices increased in:

- Perth – 99.7% of suburbs

- Adelaide – 99.0%

- Brisbane – 98.7%

- Sydney – 91.4%

- Melbourne – 80.8%

- Canberra – 71.1%

- Hobart – 59.1%

- Darwin – 59.1%

CoreLogic’s head of research, Eliza Owen, said many housing markets across the country were growing, despite high interest rates and weakening economic conditions.

“It’s often noted that Australia is not ‘one housing market’ and we’re currently seeing increased diversity in capital city market performance,” she said.

“That’s reflected in city-wide growth rates, the various levels of supply that’s available in some cities over others, and it’s reflected in the different suburbs we analyse in this report.”

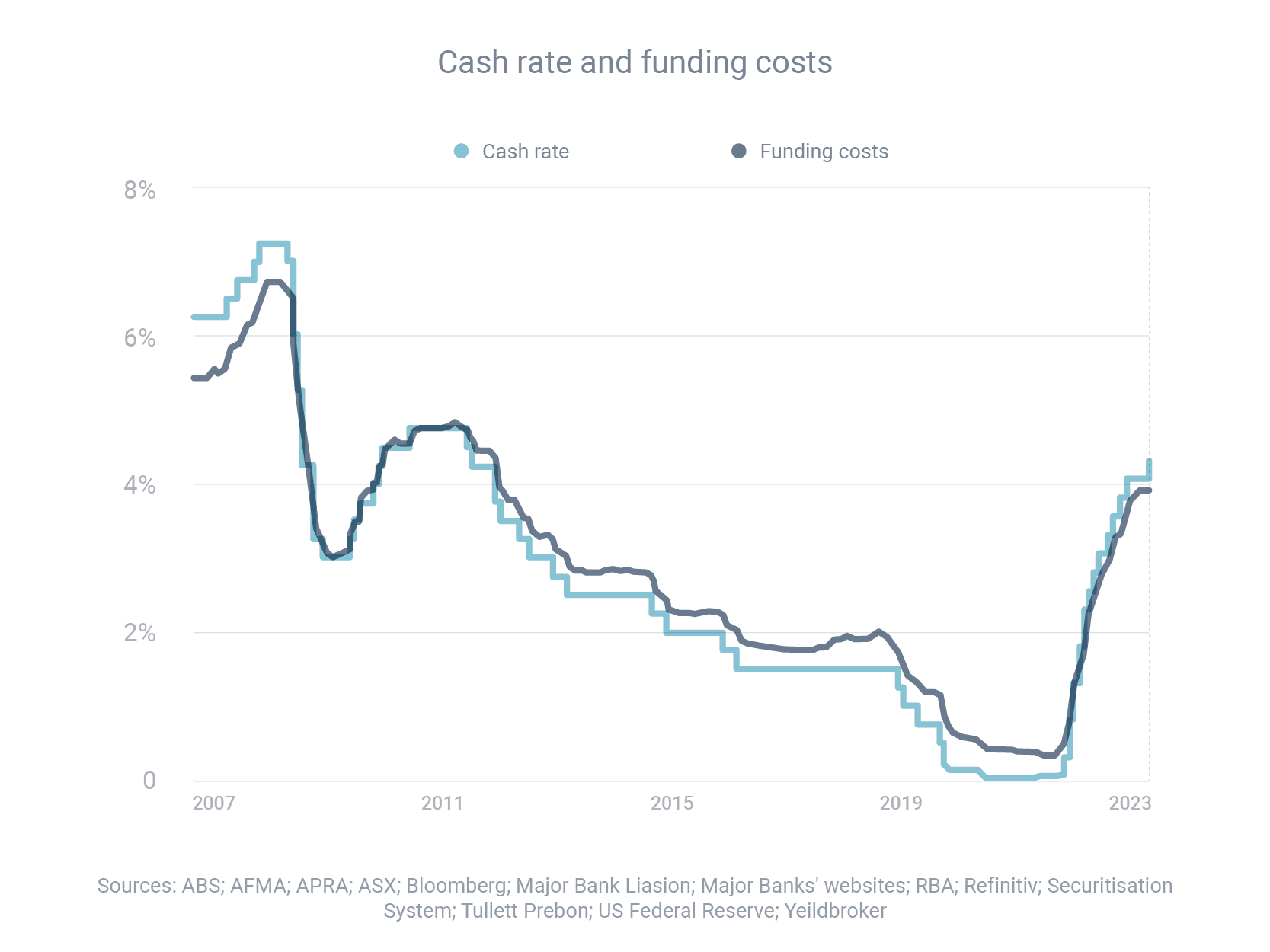

While interest rates have increased significantly over the past 18 months, this increase, thankfully, has been less than one might have expected, due to competition, according to the Reserve Bank.

Between April 2022 and September 2023, the cash rate increased by 4.00 percentage points. However, banks increased their variable rates by, on average, only 3.32 points for owner-occupiers and 3.28 points for investors. This was due, in part, to “the effect of competition between lenders on variable-rate housing loans”.

Meanwhile, banks’ funding costs increased further between the June and September quarters, which is likely to lead to higher interest rates and more pain for households.

The increase in funding costs came “as banks replaced maturing bonds issued at much lower rates and average deposit rates increased”.

Banks generally ‘buy’ funding on the wholesale market, add a margin and then on-sell this money to borrowers in the form of home loans (and other loans). So when banks’ funding costs increase, they generally have little option but to increase rates as well.

Thanks for reading. If you or your family need advice about home loans or refinancing, I'm here to help.

Kind Regards,Mark Mellick

(02) 9315 7749